The following steps show the broad strokes of initiating a Visa chargeback:

- Contact your card issuer.

- File a dispute and provide an explanation of why you’re challenging the transaction in question.

- Your request is then sent to the acquirer/card issuer of the merchant.

- The request is forwarded to the merchant.

- The merchant can either agree to pay out and refund the transaction or fight against the chargeback.

What to know about visa's New chargeback rules?

Visa's New Chargeback Rules: What You Need To Know

- Get Ready For New Chargeback Rules. If one of your customers has ever disputed a transaction, you understand how frustrating the chargeback resolution process can be.

- The "VCR" Initiative. Visa refers to its new chargeback rules as the Visa Claims Resolution ("VCR") initiative. ...

- You Are In Control. ...

What is the Visa Chargeback time limit and reason code?

Reason Code – 13.3: Previously it belonged to the reason code 53. The 120 days VISA chargeback time limit can also vary from one date to another, accordingly. Because of the leading situation, the VISA chargeback time limit is also going to begin from the time period when the card owner collected the services or products.

How does the Visa Chargeback monitoring program work?

Visa monitors your chargeback activity on a monthly basis and will notify your acquirer of any excessive chargebacks. The responsibility is then on the acquirer to work with you to help reduce your chargeback activity.

Is a chargeback the same as a refund?

Is a chargeback the same as a refund? No. Refunds are provided by the merchant in exchange for the return of a purchase. Chargebacks are forced payment reversals in which the consumer typically does not return merchandise to the merchant. The merchant will also be hit with an additional chargeback fee.

How do chargebacks work with Visa?

What Are Visa Chargebacks? When a cardholder files a dispute with the issuing bank that provides their Visa-branded credit card, the transaction becomes a Visa chargeback, also known as a Visa dispute. The bank debits the transaction amount from the merchant and gives the cardholder a temporary credit.

How do I request a chargeback on Visa?

How to Get a Visa Chargeback on Your OwnContact your Visa card issuer—this will most commonly be your bank.File a dispute and explain why you're challenging the transaction in question.Your request will be sent to the acquirer/card issuer of the merchant.More items...

How do I do a chargeback on my credit card?

How to request a chargebackYou file a chargeback request.Your card issuer reviews the dispute and will decide if it's valid or if you have to pay. ... The card network reviews the transaction and either requires your card issuer to pay or sends the dispute to the merchant's acquiring bank.More items...

Can a Visa charge be reversed?

If you or your employees notice something incorrect after submitting the authorization request, you can call your bank to stop the transaction from occurring. This is known as an authorization reversal, and it's highly preferable over a future chargeback or refund.

How long does a Visa chargeback take?

From start to finish, disputing a charge can often take 45 to 90 days. Whenever possible, however, Visa prefers to have customer disputes finalized in a month or less. This means that merchants need to respond to each phase as quickly as possible.

How long does a chargeback take?

around 30-90 daysHow Long Does the Chargeback Process Take? Depending on the reason code, issuing bank, and credit card network, the entire process usually takes around 30-90 days. Cases that go to arbitration will take longer.

Can you go to jail for chargebacks?

Can you go to jail for disputing charges? It's technically possible, as friendly fraud can be considered a form of wire fraud. However, this only happens in extreme cases. In general terms, it's practically unheard of for cardholders to end up behind bars for committing friendly fraud.

Are chargebacks always successful?

You might not always get a fair outcome when you dispute a chargeback, but you can increase your chances of winning by providing the right documents. Per our experience, if you do everything right, you can expect a 65% to 75% success rate.

Can a chargeback be denied?

Can a Chargeback Be Denied? Yes. If the cardholder doesn't make a compelling enough case to their bank, or doesn't have a valid reason for filing a chargeback, the bank may refuse to open a dispute. Merchants can also provide evidence refuting a chargeback.

Will a chargeback hurt my credit?

A chargeback does not usually affect your credit. The act of filing a chargeback because of a legitimate cause for complaint against a business won't affect your credit score. The issuer may add a dispute notation to your credit report, but such a notation does not have a negative effect on your credit.

When should you chargeback?

It's appropriate to file a credit card chargeback if:01 | A transaction on your statement was fraudulent. ... 02 |An item you ordered was never delivered. ... 03 |An item was damaged on arrival. ... 04 |Incorrect transaction amount. ... 05 | Charged for canceled subscription. ... 01 | A chargeback might be more convenient.More items...•

Does chargeback hurt your credit?

A chargeback does not usually affect your credit. The act of filing a chargeback because of a legitimate cause for complaint against a business won't affect your credit score. The issuer may add a dispute notation to your credit report, but such a notation does not have a negative effect on your credit.

Do customers always win chargebacks?

Chargebacks are easy to initiate and are often successful, but they don't cover all scenarios. Chargebacks are designed as a last resort; the first step should generally be to try to resolve the issue with the merchant directly.

How long do you have to do a chargeback on credit card?

120 daysEach card network and issuing bank sets its own time limits for filing a chargeback. However, the legal minimum time limit for filing a chargeback in the United States is 60 days, and most banks give cardholders 120 days to dispute a charge.

Is a chargeback the same as a refund?

In the case of a refund, the merchant gives the customer the money back directly after the return or exchange of a product or report of dissatisfaction with a service. For chargebacks, the consumer receives credit from his or her card issuer.

What is chargeback on Visa?

Chargeback allows you to ask your card issuer to reverse a transaction on your credit or debit card. By requesting a chargeback, you’re disputing the transaction in question and asking to get your money back. How can you initiate a chargeback on your Visa card?

What Is the Visa Chargeback Policy?

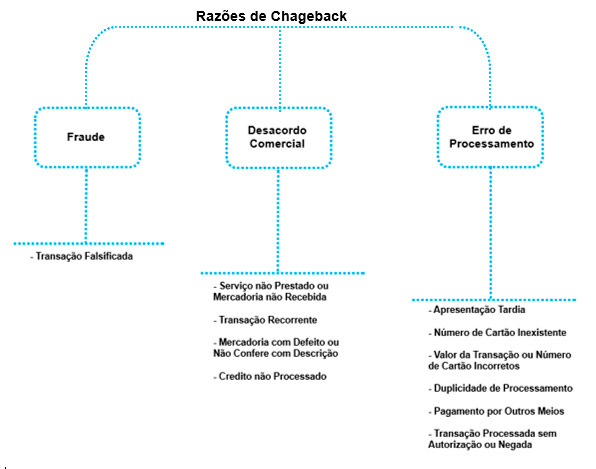

In its guide called Chargeback Management Guidelines for Visa Merchants, Visa singled out three main reasons for a chargeback:

What Are the Visa Dispute Categories?

Visa specifies four main dispute categories that come with a subset of specific codes. Each code is assigned to a different reason for a chargeback request.

How long does it take for a Visa chargeback to be resolved?

They can use this time to try to dispute the transaction again. If a second chargeback is filed, Visa will make the final decision, typically within ten days.

How long does a merchant have to respond to a chargeback request?

They will have up to 120 days if the chargeback request is related to fraud or duplicate processing. After the customer submitted the claim, the merchant will have 30 days to defend themselves and respond with compelling evidence against the chargeback request.

What is a visa?

Visa is a U.S.-based multinational company that specializes in financial services. The firm facilitates transfers of electronic funds worldwide, primarily through their Visa-branded credit cards, debit cards, and prepaid cards. Visa does not issue cards but supplies financial institutions such as banks with payment products that are then offered to that institution’s customers.

What happens if you don't dispute a credit card charge?

If they don’t, he or she will immediately lose the dispute, and they will have to give the money back. If you’re not sure what to do, you can reach the bank’s customer service by dialing the number on the back of your credit card and tell the rep that you want to initiate a chargeback or dispute a charge.

What is a chargeback on a credit card?

A chargeback lets you dispute a credit card transaction and reverse it, getting your money back. For example, if you paid a subscription fee to MoviePass and the company just won’t let you cancel your subscription, you can do a chargeback. The chargeback process is handled entirely through your bank or credit card issuer.

How does a chargeback work?

The chargeback process is handled entirely through your bank or credit card issuer. The issuer will contact the business and sort things out, and you should almost certainly win if you have a valid reason for the chargeback.

What About Debit Cards?

You have more consumer protections when you use a credit card for purchases. In the US, you have rights to dispute transactions under the Truth in Lending Act and Fair Credit Billing Act —but only when using a credit card. For example, under the Fair Credit Billing Act, you have up to sixty days to dispute a transaction after the statement is mailed to you. Credit card companies may give you more time, but that’s the minimum required by law.

What happens if you get charged twice for the same thing?

You were charged twice for the same thing: If you see duplicate transactions on your card and the merchant only should have charged you once, you can initiate a chargeback to get rid of them.

How much does a merchant have to pay for a chargeback?

The merchant will have to pay a sizable fee—perhaps $20 to $50 —if you win a chargeback dispute. It’s in the business’s interest to fix your problem before your credit card company gets involved. But, if the merchant refuses to work with you—perhaps it sent a counterfeit product and is refusing to refund you, or maybe it isn’t providing ...

How long does it take to get money back if you don't get a credit card?

You often have up to 120 days to initiate a chargeback, but the time limits can vary a bit depending on the type of chargeback.

What happens if you don't enter your pin on a debit card?

If your debit card ran as “credit”—in other words, if you didn’t enter your PIN while making the purchase—your bank has to follow the same Visa or Mastercard rules for handling a dispute. If it ran as debit—in other words, if you entered the PIN when making a purchase—the process likely wouldn’t be as easy for you.

How Do Visa Chargebacks Work?

Much like other chargebacks, Visa chargebacks start with a cardholder disputing a charge with their issuing bank. If the bank approves a chargeback, the merchant can either accept the chargeback or fight it through representment.

What Are Visa Chargebacks?

When a cardholder files a dispute with the issuing bank that provides their Visa-branded credit card, the transaction becomes a Visa chargeback, also known as a Visa dispute. The bank debits the transaction amount from the merchant and gives the cardholder a temporary credit.

What Are Visa's Dispute Categories?

Visa specifies four dispute categories that encompass its various chargeback reason codes: Fraud, Authorization, Processing Errors, and Consumer Disputes.

How Can Merchants Prevent Visa Disputes?

Merchants can prevent Visa disputes by using a clear and recognizable billing descriptor , offering helpful and available customer service, and using effective fraud prevention tools.

What Is the Compelling Evidence Requirement for Visa Disputes?

Generally speaking, compelling evidence in chargeback representment will consist of proof that the cardholder knowingly participated in the transaction and received the intended benefit thereof.

Why do credit card companies charge back?

The existence of chargebacks allows cardholders to feel more confident about making purchases with their credit cards, knowing that they won’t be held responsible for the actions of identity thieves, deceptive merchants, and other fraudsters . However, the chargeback process also has loopholes that can be exploited, allowing cardholders to commit so-called “friendly fraud,” when they obtain a chargeback by making false claims, sometimes unknowingly, but often intentionally.

What happens if a merchant accepts a chargeback?

If the issuer accepts the merchant’s evidence, they will reverse the chargeback. If one or more parties involved in the chargeback do not accept the outcome at this point, they may file for arbitration, at which point Visa will decide the matter.

How Long Do Merchants Have to Respond to a Visa Dispute?

The Visa chargeback process is broken into phases. Merchants must respond within 30 days of day one for each phase. In Visa’s case, day one is the day after each phase is initiated. Merchant time limits have only one exception: if either party wants to escalate a dispute to arbitration, they must do so within 10 days.

How long does it take to dispute a Visa card?

The deadlines are pretty straightforward on the consumer side. From the original transaction or expected delivery date, Visa cardholders have no more than 120 days to file a dispute. There are a few exceptions, which we’ll cover later in this post. In most situations, though, 120 days is the rule.

What is Visa reason code 13.6?

Visa reason code 13.6 deals with chargebacks stemming from a credit not being processed. Issuers must wait 15 calendar days from the credit transaction receipt date before initiating a dispute, unless doing so would cause the dispute to exceed the time limit.These dispute must be processed no later than 120 calendar days from either:

Do Visa chargebacks only apply to merchants?

Another thing to keep in mind is that the Visa chargeback time limits presented here don’t only apply to merchants. Other parties, such as acquirers and processors, may also have actions to perform in the same timeframe. They have the power to move up deadlines to give themselves more time.

Do Visa chargebacks have time limits?

Are you a merchant fighting an unfair chargeback claim? Or, are you a cardholder dealing with a case of criminal fraud? In either case, Visa chargebacks come with built-in time limits you need to know about. Each phase of the dispute process has a specific deadline for action. Waiting too long could mean than you forfeit your chargeback rights ..

Does Visa chargeback require a response?

Responses are mandatory in all cases. At one point, Visa allowed merchants to ignore the dispute until after the deadline, effectively accepting the chargeback by default. Now, though, Visa imposes a fine on non-response, even if that response is to accept the chargeback.

What is chargeback in credit card?

A “chargeback” provides an issuer with a way to return a disputed transaction. When a cardholder disputes a transaction, the issuer may request a written explanation of the problem from the cardholder and can also request a copy of the related sales transaction receipt from the acquirer, if needed. Once the issuer receives this documentation, the first step is to determine whether a chargeback situation exists. There are many reasons for chargebacks—those reasons that may be of assistance in an investigation include the following: • Merchant failed to get an authorization • Merchant failed to obtain card imprint (electronic or manual) • Merchant accepted an expired card When a chargeback right applies, the issuer sends the transaction back to the acquirer and charges back the dollar amount of the disputed sale. The acquirer then researches the transaction. If the chargeback is valid, the acquirer deducts the amount of the chargeback from the merchant account and informs the merchant. Under certain circumstances, a merchant may re-present the chargeback to its acquirer. If the merchant cannot remedy the chargeback, it is the merchant’s loss. If there are no funds in the merchant’s account to cover the chargeback amount, the acquirer must cover the loss.

What is chargeback management?

The Chargeback Management Guidelines for Visa Merchants contains detailed information on the most common types of chargebacks merchants receive and what can be done to remedy or prevent them. It is organized to help users find the information they need quickly and easily. The table of contents serves as an index of the topics and material covered.

How to get a copy of a credit card transaction?

When a card issuer sends a copy request to an acquirer, the bank has 30 days from the date it receives the request to send a copy of the transaction receipt back to the card issuer. If the acquirer sends the request to you, it will tell you the number of days you have to respond. You must follow the acquirer’s time frame. Once you receive a copy request, retrieve the appropriate transaction receipt, make a legible copy of it, and fax or mail it to your acquirer within the specified time frame. Your acquirer will then forward the copy to the card issuer, which will, in turn, send it to the requesting cardholder. The question or issue the cardholder had with the transaction is usually resolved at this point. Note: When you send the copy to the acquirer, use a delivery method that provides proof of delivery. If you mail the copy, send it by registered or certified mail. If you send the copy electronically, be sure to keep a written record of the transmittal.

How long does it take to get a copy of a card receipt?

When a card issuer sends a copy request to an acquirer, the bank has 30 days from the date it receives the request to send a copy of the transaction receipt back to the card issuer. If the acquirer sends the request to you, it will tell you the number of days you have to respond. You must follow the acquirer’s time frame.

Why monitor chargeback rates?

Monitoring chargeback rates can help merchants pinpoint problem areas in their businesses and improve prevention efforts. Card-absent merchants may experience higher chargebacks than card-present merchants as the card is not electronic read, which increases liability for chargebacks.

What is Visa fraud?

The Visa Merchant Fraud Program monitors chargeback activity for all U.S. acquirers and merchants on a monthly basis. If a merchant meets or exceeds specified chargeback thresholds, its acquirer is notified in writing.

How to check your DBA?

You can check this information yourself by purchasing an item on your Visa card at each of your outlets and looking at the merchant name and location on your monthly Visa statement. Is your name recognizable? Can your customers identify the transactions made at your establishment?

What causes a chargeback on a credit card?

This is referred to as a bank chargeback, and may be caused by late presentment, duplicate processing, an expired card, or merchant fraud.

Who will review chargeback information?

The acquiring bank will electronically re-present the chargeback dispute information to the issuing bank, who will then review the information. One of three things will happen:

What is chargeback system?

The concept of the chargeback system is relatively simple: if a Cardholder has an issue with a transaction that cannot be resolved dealing directly with the Merchant, then said Cardholder can appeal directly to the Card Network.

What is the outcome of a chargeback dispute?

Ultimately, the outcome of each chargeback dispute is determined by humans, who are largely free to interpret regulations and issue judgments as they see fit. The chargeback process is outdated. Chargebacks were devised in a pre-internet era.

Why do banks use reason codes?

Theoretically, chargeback reason codes help you understand the cause for the chargeback and determine the best way to validate the original transaction. However, reason code intelligence isn’t as helpful as it should be. Banks assign reason codes based on cardholders’ claims, making it easy for the bank to be deceived into facilitating friendly fraud chargebacks. Then, without understanding the true chargeback trigger, you can’t deploy the proper dispute or prevention tactics.

What is the issuer of a credit card?

Issuer: The bank who issued the card to the cardholder.

What are the key players involved in a transaction?

There are several key players involved, including: Cardholder: The owner of the card involved in a transaction. Merchant: The party who sold the goods or services being disputed. Issuer: The bank who issued the card to the cardholder. Acquirer: The bank tasked with acquiring payment on the merchant’s behalf.

How to chargeback a Visa card?

To start the chargeback process, contact your bank and they will walk you through what needs to be done. The following steps show the broad strokes of initiating a Visa chargeback: 1 Contact your card issuer. 2 File a dispute and provide an explanation of why you’re challenging the transaction in question. 3 Your request is then sent to the acquirer/card issuer of the merchant. 4 The request is forwarded to the merchant. 5 The merchant can either agree to pay out and refund the transaction or fight against the chargeback.

What is a chargeback on a credit card?

The chargeback process lets you dispute a charge made on your credit or debit card and ask your card issuer to reverse the transaction. Essentially, you disputing the validity of the transaction and request to get your money returned. However, keep in mind that a chargeback is not the same thing as a refund. Chargebacks should not be attempted in ...

What happens if a merchant takes a chargeback to arbitration?

Plus, if a merchant takes the chargeback to the arbitration stage and wins the case, the associated chargeback fee might pass to you (depending on your bank). Lastly, the more chargebacks a merchant receives, the more they pay in fees.

How to start a chargeback?

Instead, a chargeback should be filed only after all efforts have been exhausted to get the merchant to cooperate. To start the chargeback process, contact your bank and they will walk you through what needs to be done.

What happens if a bank charges you for illegitimate charges?

If the bank learns that an illegitimate chargeback was filed, you run the risk of your account being terminated. This could make it hard to find banking services and could negatively impact your credit score. Plus, if a merchant takes the chargeback to the arbitration stage and wins the case, the associated chargeback fee might pass to you ...

How to return a product to a seller?

Your first course of action should be to contact the merchant directly and attempt to initiate a return. The seller’s return policies should be listed on their site. They should also be linked in the order confirmation email sent to you before the goods arrived. This document will outline their refund requirements, such as a deadline, or whether tags are required.

How long does it take to get your money back from eConsumer?

Our process is quick and painless. We’ll provide you with a claim form to fill out that can be completed in five minutes, and it doesn’t require any sensitive account information. Once you’ve filed a claim, we can get your money back quickly – usually within 24 hours or less.